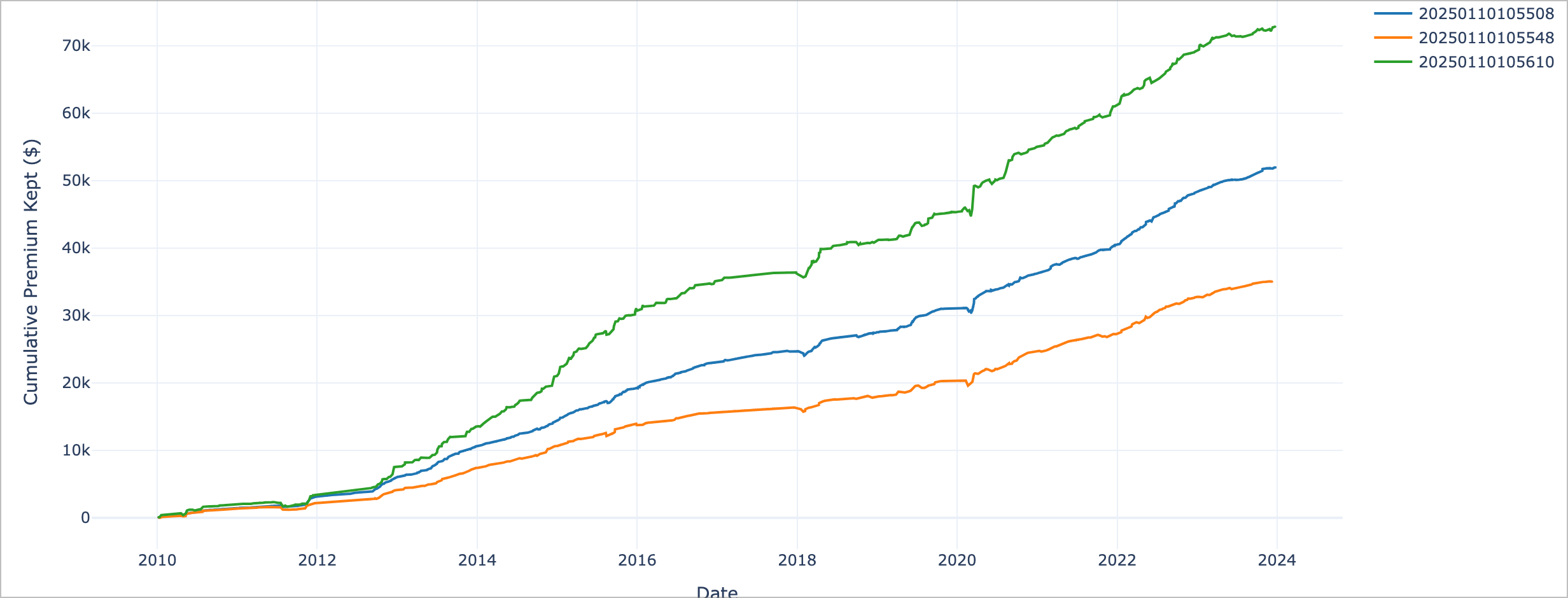

Short Straddles with Laddering

Short Straddles

For e.g. Given that our account can trade 5 SPX contracts at once.

- We can either trade 1 contract every day - 5 different positions

- Or we can trade all 5 contracts at the same time in a single trade - 1 position

- Or we can stagger 5 contracts in a single trade. Add 1 contract every day

Here are the results

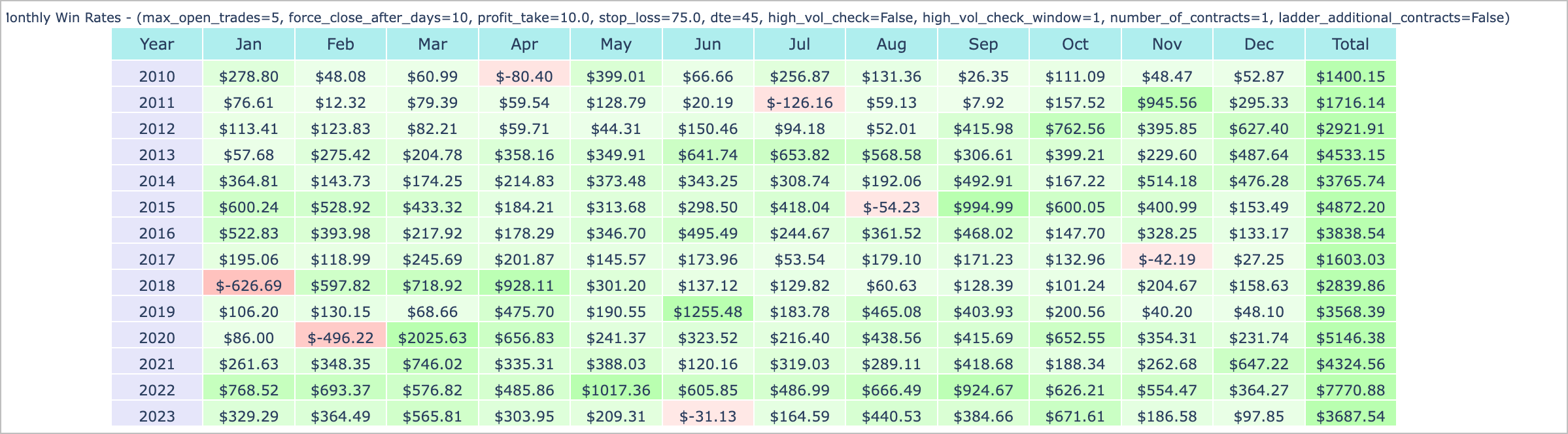

(a) 1 Contract Every Day (Max 5 Positions) > 45 DTE Expiry

(b) Ladder positions over time. Add 1x every day until we have 5 contracts on a single expiry.

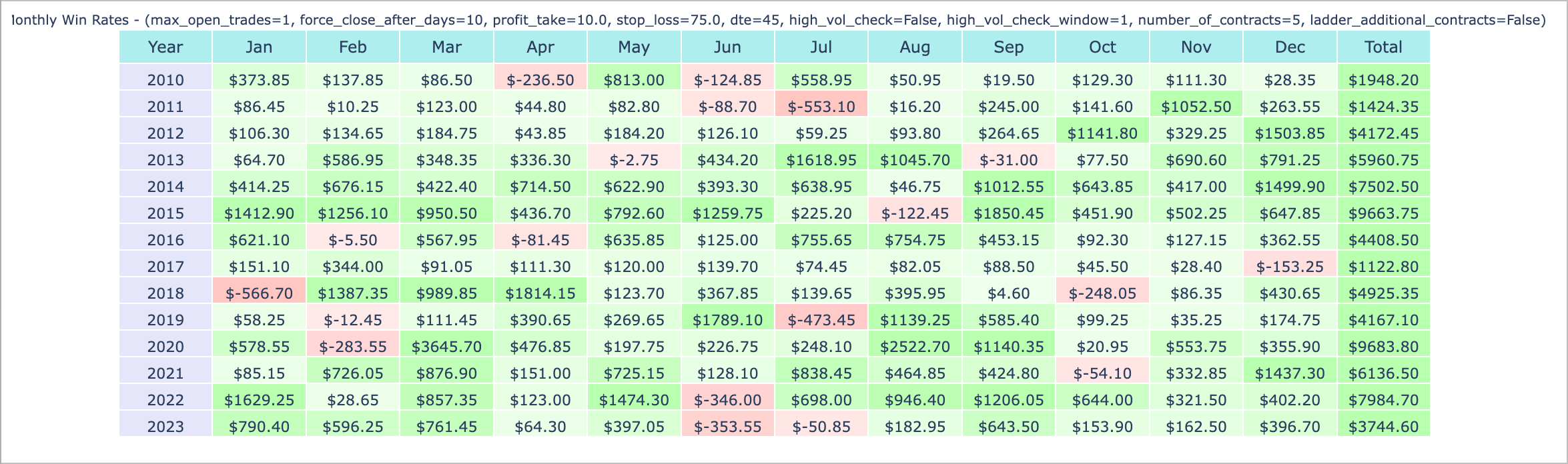

(c) Use all 5 contract at once on a single trade.

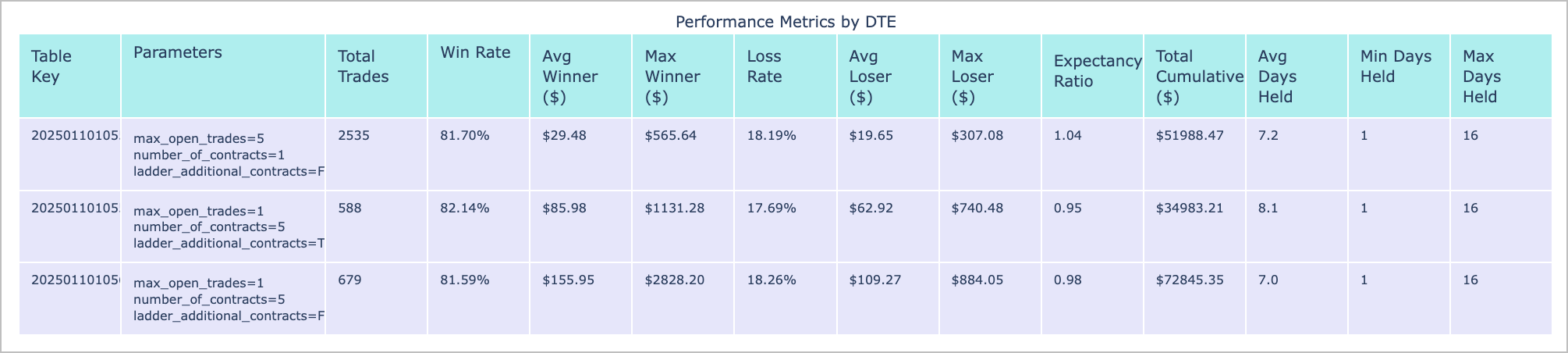

(a) looks better in terms of expectancy ratio and drawdowns. Even though the overall returns are much better with (c)

Complete table

(a) => Blue

(b) => Orange

(c) => Green